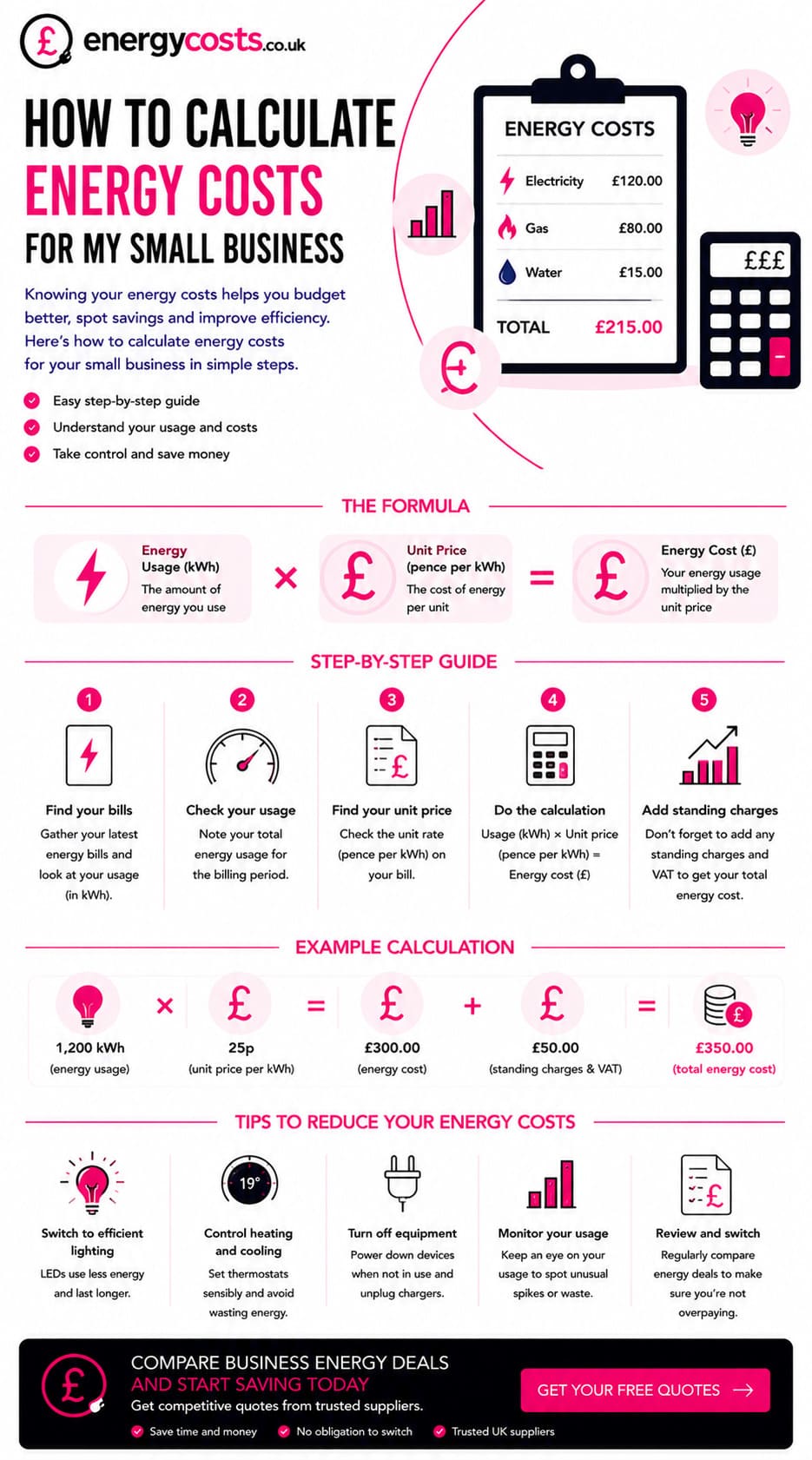

Understanding how to calculate your energy costs is essential for small businesses. It helps with budgeting, identifying savings opportunities, and negotiating better deals. While energy bills can appear complex, breaking them down into their key components makes it easier to see exactly what you’re paying for.

What makes up your energy bill?

Business energy bills usually include:

- Unit rate (kWh) – the cost per kilowatt-hour of electricity or gas your business uses.

- Standing charge – a daily fee to cover network and supply costs, paid regardless of usage.

- VAT – usually 20%, but some small businesses may qualify for 5% if usage is low or if energy is partly used for domestic purposes.

- Other charges – such as government levies, environmental schemes, and Climate Change Levy (CCL) for non-domestic energy use.

Step-by-step: calculating your small business energy costs

1. Work out your usage

Check your meter readings or bills for your annual consumption in kilowatt-hours (kWh). If you’re a new business, use industry averages:

- Small office: 10,000–15,000 kWh electricity per year

- Small shop: 7,000–11,000 kWh electricity per year

- Small café: 15,000–25,000 kWh gas per year

2. Multiply by your unit rate

If your unit rate is, for example, 30p per kWh for electricity and your business uses 12,000 kWh annually, your energy usage cost is:

12,000 x £0.30 = £3,600 per year

3. Add standing charges

If your standing charge is 50p per day, that adds:

£0.50 x 365 = £182.50 per year

4. Apply VAT and levies

Add 20% VAT (or 5% if eligible) and any government charges such as the CCL. This gives you the total estimated annual bill.

Example calculation

- Annual usage: 12,000 kWh at £0.30 = £3,600

- Standing charge: £0.50 per day = £182.50

- Subtotal = £3,782.50

- VAT at 20% = £756.50

- Total = £4,539 per year

Tips to keep costs down

- Compare suppliers regularly to find better tariffs.

- Install smart meters to track consumption more accurately.

- Identify energy-hungry equipment and invest in efficient alternatives.

- Train staff to adopt energy-saving practices.

Gas: converting m³ or ft³ to kWh (with worked example)

Most business gas meters measure volume (cubic metres m³ for metric meters, or cubic feet ft³ for older imperial meters), but bills charge you in kWh. Suppliers convert your meter units into kWh using a standard method set out in UK regulations, and the steps shown on GOV.UK match what you’ll see on most bills.

Metric meter (m³) conversion to kWh

- Units used (m³) = current reading − previous reading

- kWh = units used × calorific value × 1.02264 ÷ 3.6

- Calorific value (CV) is shown on your bill (typically within the 38–41 MJ/m³ range).

- 1.02264 is a correction factor for temperature/pressure.

- Dividing by 3.6 converts megajoules to kWh.

Imperial meter (ft³) conversion to kWh

If your meter reads in cubic feet, you convert to m³ first:

- m³ = ft³ × 0.0283 (or if your reading is in hundreds of cubic feet, multiply by 2.83)

Then apply the same kWh formula above.

Worked example (metric meter)

- Units used: 250 m³

- Calorific value: 39.5 MJ/m³ (example CV)

- kWh = 250 × 39.5 × 1.02264 ÷ 3.6

- kWh ≈ 250 × 39.5 = 9,875

- 9,875 × 1.02264 ≈ 10,098.6

- 10,098.6 ÷ 3.6 ≈ 2,805 kWh

Once you have the kWh figure, you can calculate the energy charge by multiplying by your gas unit rate (and then adding standing charges, VAT, and any other bill items).

Don’t forget climate change levy (CCL)

Many UK business energy bills include Climate Change Levy (CCL) as a separate line item (or it may be incorporated into the unit rate, depending on the supplier and tariff). From 1 April 2026, the main CCL rate for both electricity and natural gas is £0.00801 per kWh.

A simple way to estimate the levy element is:

Estimated CCL (£) = kWh used × 0.00801

Example: 10,000 kWh × 0.00801 = £80.10 (CCL element)

Some organisations can pay reduced CCL rates if they’re covered by a Climate Change Agreement (CCA), but most small businesses pay the main rate.

VAT: the reduced rate thresholds for small usage (and why they matter)

Business energy is often charged at the standard VAT rate, but HMRC allows the reduced VAT rate to apply in certain cases, including where the supply is a small (de minimis) quantity at a single premises.

Electricity de minimis threshold (per premises)

If you use no more than an average of:

- 33 kWh per day, or

- 1,000 kWh per month,

the supply can be treated as reduced-rated VAT for that premises.

HMRC also sets a comparable de minimis concept for gas (often referenced alongside the electricity threshold) of 145 kWh per day. (GOV.UK)

Where usage is above the de minimis limits, VAT treatment depends on whether the energy is for qualifying or non-qualifying use, and some businesses may need to confirm their position to their supplier for the correct VAT rate to be applied.

FAQ – How to calculate energy costs for my small business

You can lower kWh consumption by switching to LED lighting, servicing heating and cooling systems regularly, and encouraging staff to turn off equipment when not in use. Even small changes add up over time.

On average, a small business spends £3,000–£7,000 per year on electricity and gas, depending on the sector. Costs vary based on location, usage, and the contract agreed with the supplier.

Yes. If your business uses less than 33 kWh of electricity or 145 kWh of gas per day, or if part of your energy use is domestic (e.g., in a guest house), you may qualify for 5% VAT.

A standing charge is a fixed daily fee paid to cover the cost of maintaining the energy supply network. It applies regardless of how much energy your business consumes.

Yes. Smart meters give real-time usage data, helping businesses track consumption patterns and identify inefficiencies. This visibility can make it easier to reduce waste and negotiate better tariffs.